The closure of the Strait of Hormuz has collided with a European polyol industry already operating under severe structural pressure, squeezed by low-priced Asian imports, shuttered domestic capacity, and energy costs far above those faced by competitors in Asia or the Middle East. The market, in the words of one participant this week, is “muy nervioso.”

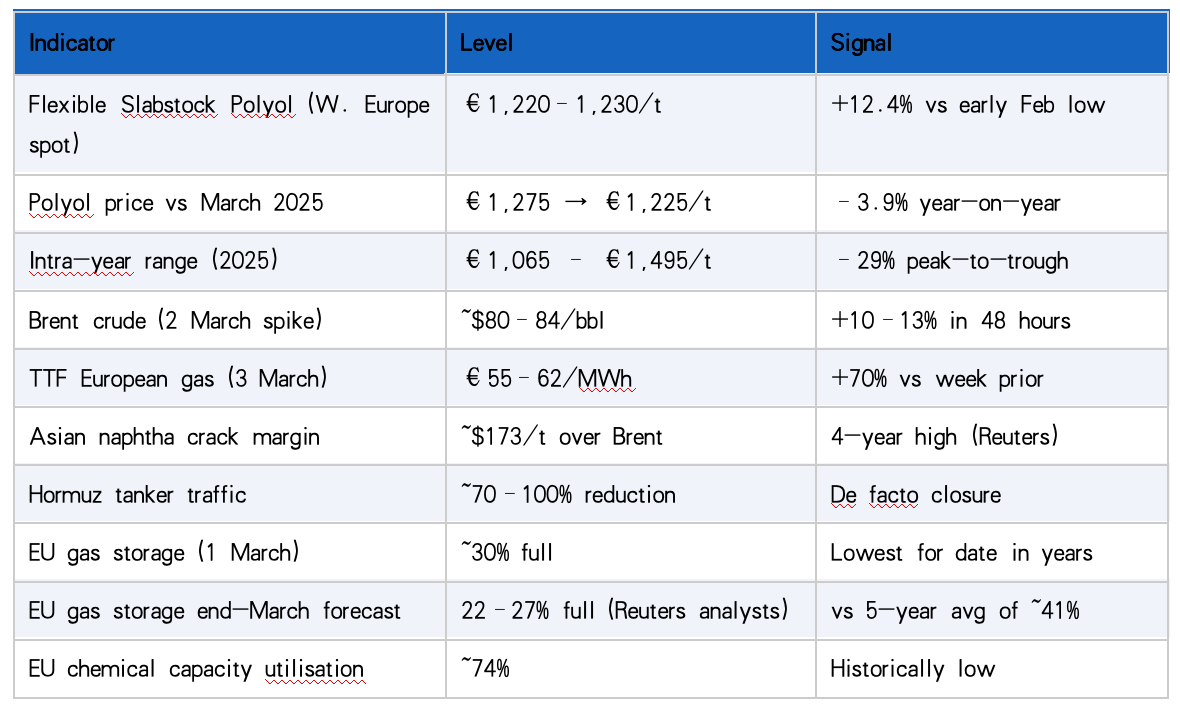

MARKET SNAPSHOT — 5 MARCH 2026

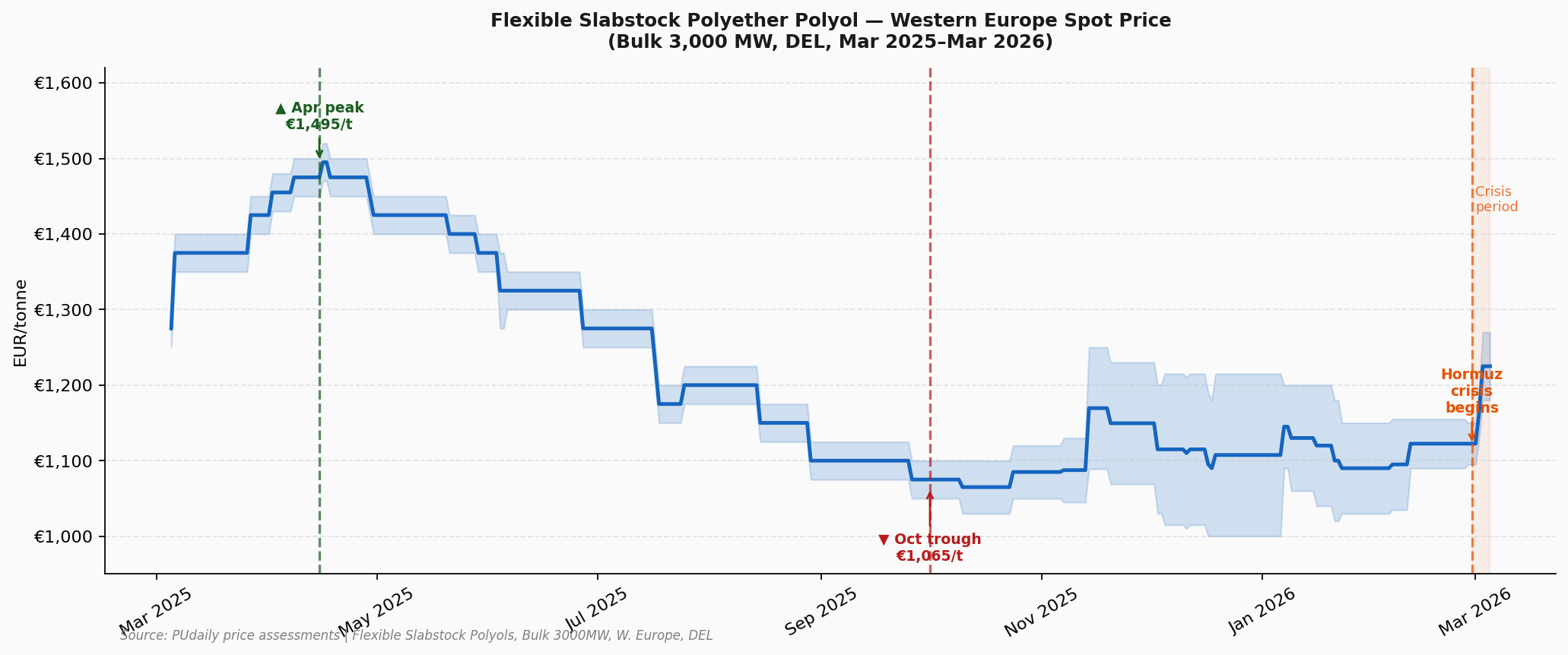

PRICE TRAJECTORY: TWELVE MONTHS OF STRUCTURAL PRESSURE

The chart below captures the industry’s recent price trajectory. Spot prices for flexible slabstock polyol in Western Europe opened March 2025 at €1,275/t and rallied sharply to €1,495/t in mid-April on seasonal restocking. Prices then declined steadily, falling nearly 29% to a trough between €1,000 and €1,065/t by early October, a level at which most non-integrated European producers operate at very tight margins.

Chart 1 — Flexible Slabstock Polyol spot price (mid-range), Western Europe, Mar 2025–Mar 2026.

Source: PUdaily price assessments.

THE INDUSTRY BEFORE THE CRISIS: ALREADY UNDER STRUCTURAL PRESSURE

Before a single missile was launched or a tanker rerouted, the European polyether polyol sector was already facing significant structural disadvantages that years of industry lobbying had failed to resolve. Understanding this baseline is essential to explaining why the current crisis may represent more than a temporary disruption.

European chemical producers have operated with a persistent energy cost disadvantage compared with global peers. Throughout 2024 and 2025, gas prices in Europe remained several times higher than in the United States. Data from the European Chemical Industry Council (Cefic) indicate that at the start of 2025, European gas prices were approximately 3.3 times higher than those in the US.

For an energy-intensive process such as polyether polyol production, which requires propylene oxide feedstock and significant utilities for reactor temperature control, energy pricing is not a marginal cost factor. It represents a structural competitive constraint that compounds whenever feedstock costs increase.

Trade statistics also illustrate growing competitive pressure. EU customs data show that between 2023 and 2025 import volumes increased while average unit values declined. The practical result is a price ceiling on commodity grades of polyether polyols.

European producers cannot sustainably price above the landed cost of imported Asian material, yet their production costs frequently exceed that level at non-integrated sites. This dynamic has placed persistent downward pressure on margins.

2025: the year of capacity rationalisation

The market response to this structural squeeze has been a wave of closures and production rationalisations that have significantly reduced Europe’s shock-absorption capacity.

Dow Chemical confirmed the shutdown of its Tertre (Belgium) polyols facility, representing approximately 94,000 t/year of commodity-grade capacity, citing energy costs, regulatory pressures, and sustained import competition. The site is expected to cease operations by the end of March 2026.

INEOS closed propylene oxide and propylene glycol production at its Cologne site on an indefinite basis, signalling a structural adjustment rather than a temporary market response.

LyondellBasell and Covestro also confirmed the permanent closure of the PO/SM “PO11” unit at Maasvlakte in Rotterdam, referencing global overcapacity and Europe’s cost disadvantage.

These closures reduce Europe’s ability to buffer supply disruptions and weaken the economic case for maintaining integrated propylene oxide supply chains within the region.

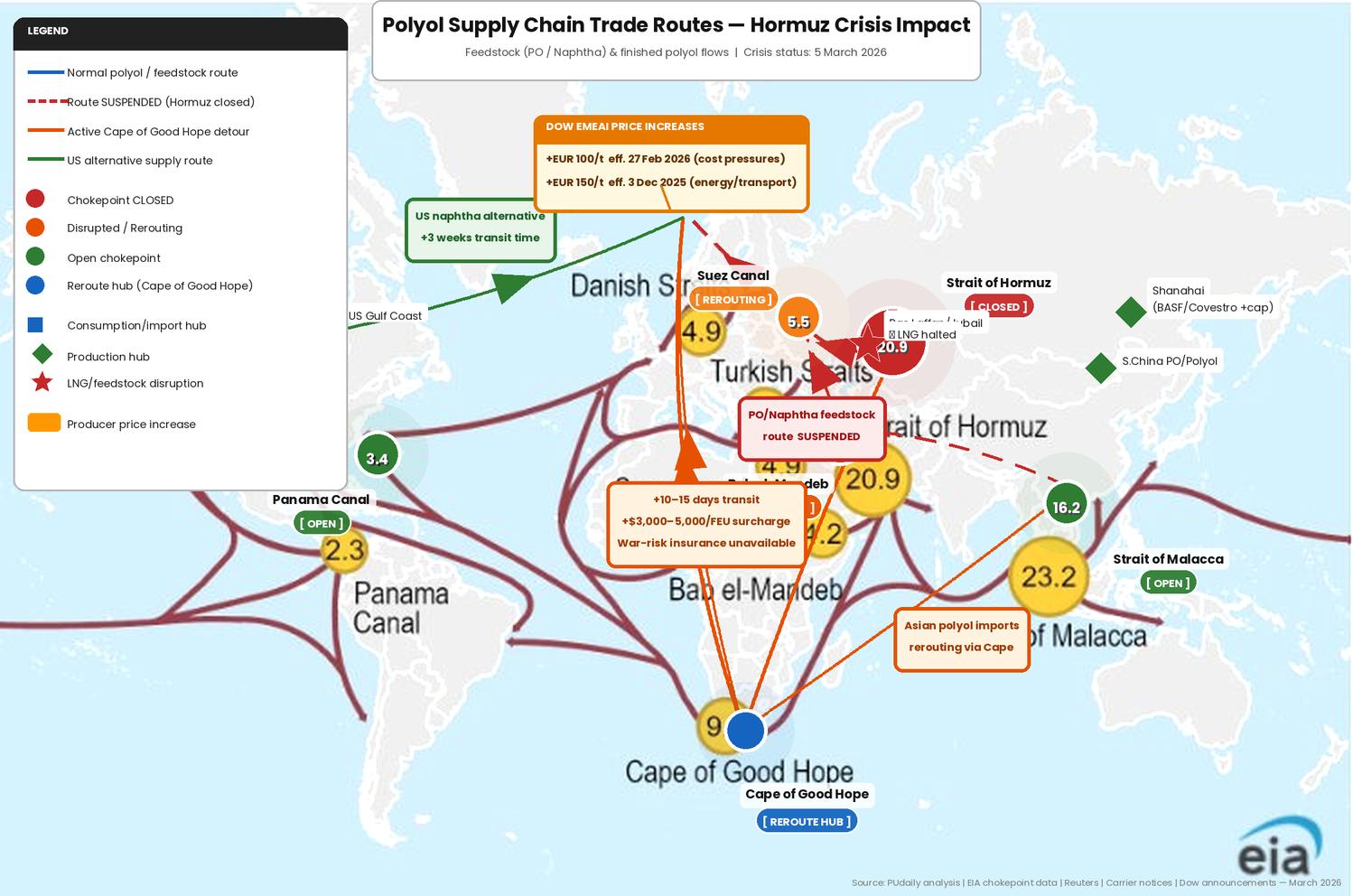

THE HORMUZ SHOCK: THREE TRANSMISSION CHANNELS

The military escalation involving Iran that began at the end of February 2026 has disrupted the European polyol supply chain through three simultaneous channels. Individually, each would be manageable. Combined, they create significant uncertainty across the market.

Map, Global petrochemical trade routes and chokepoint status as of 5 March 2026. Red dashed = suspended (Hormuz closure); orange = active Cape of Good Hope detours; green = US alternative. Dow EMEAI price increases annotated.

Source: PUdaily analysis, EIA, carrier notices.

Major shipping companies including Maersk, MSC, CMA CGM and Hapag-Lloyd have suspended transits through the Strait of Hormuz. Vessels are being rerouted around the Cape of Good Hope, adding approximately 10–15 days to transit times and triggering emergency freight surcharges.

War-risk insurance has either become unavailable or prohibitively expensive. Reports indicate that several vessels have been struck near the strait and shipping intelligence suggests that a large number of vessels remain stranded in the surrounding area.

CMA CGM has introduced emergency conflict surcharges of up to $4,000 per container. For polyols transported in ISO tanks or bulk shipments, the per-tonne freight impact follows a similar logic.

Buyers who in recent years reduced inventories and relied on just-in-time imports from Asia or the Middle East now face supply chain vulnerability. Market participants report rising freight rates, although confirmed figures remain limited as the situation continues to evolve.

The energy dimension of the crisis may have even deeper structural implications. QatarEnergy suspended LNG production following strikes affecting facilities at Ras Laffan and Mesaieed. Qatar supplies roughly 20% of global LNG, and the disruption immediately tightened global gas markets.

European gas storage levels were already relatively low for this time of year, around 30%. As supply concerns intensified, TTF futures rose sharply, increasing approximately 70% within days and peaking above €60/MWh. Some market estimates suggest that under a sustained one-month Hormuz disruption scenario, TTF prices could approach €70–€75/MWh.

For polyol producers whose margins were already thin before the crisis, such energy cost increases represent a severe economic challenge. Each increase in gas prices directly erodes margins in a market where selling prices remain constrained by international competition.

PRIMARY SOURCE — DOW EUROPE: PRICE INCREASE ANNOUNCEMENTS

3 December 2025 — Dow Europe GmbH announced an immediate increase of +€150/t for all polyether polyol grades in EMEAI (Europe, Middle East, Africa, India), effective immediately or within shortest time permitted by contract. Dow cited escalating raw material, energy, and transportation costs pressuring production economics.

27 February 2026 — Dow Europe announced a further +€100/t increase for all polyether polyol series in EMEAI, effective immediately. Dow cited current cost pressures and evolving supply-demand dynamics — the announcement landing one day before the outbreak of military conflict in Iran on 28 February, which further intensified expectations among polyurethane raw material suppliers.

Combined announced increase: +€250/t since December 2025. Source: PUdaily, Dow Europe GmbH announcements.

The naphtha disruption is affecting multiple regions simultaneously. Asian petrochemical producers are also facing feedstock supply risks as Middle Eastern export flows are disrupted.

Reports indicate that several Asian petrochemical companies are considering run rate reductions or temporary shutdowns. Indonesia’s Chandra Asri has declared force majeure on certain contracts, while Japanese producers have cancelled import tenders for April naphtha cargoes.

Asia typically imports around four million tonnes of Middle Eastern naphtha per month. South Korea alone sources roughly 54% of its naphtha supply through routes that pass the Strait of Hormuz.

If Asian steam crackers begin reducing operating rates due to feedstock constraints, this could temporarily reduce export pressure on European markets. However, the impact would depend on how long the disruption persists and how quickly alternative supply routes are secured.

THE MARGIN SQUEEZE: SCENARIO ANALYSIS

Even under rapid geopolitical de-escalation, many European producers remain only marginally profitable on commodity grades.

Under prolonged disruption, the gap between production costs and achievable selling prices may widen further, compressing margins to levels that historically have triggered additional plant closures or force majeure declarations.

The key dynamic is asymmetry. Cost shocks related to energy, logistics, and feedstocks transmit rapidly and with high certainty. Price recovery, however, is constrained by the competitive ceiling imposed by imports.

Even if Asian producers experience their own cost increases, they often have greater scale, integration, and alternative supply options that allow them to absorb temporary margin compression more easily.

IMPLICATIONS FOR MARKET PARTICIPANTS

For polyurethane processors, including foam, automotive, and insulation producers, security of supply is rapidly becoming a priority alongside price management. Buyers that have relied heavily on spot imports and minimal inventories face the greatest risk of supply disruption.

Market participants report increasing concern about availability, which may drive precautionary inventory building in the near term. Buyers with long-term supply contracts or domestic supplier relationships are comparatively better positioned.

The arbitrage trade that has been profitable for the past 18 months, Asian polyol into Europe on improving freight and weak spot prices, is temporarily shut. Logistics are disrupted, insurance is expensive or unavailable, and transit times have extended. Traders who have cargo already en route face uncertainty about delivery timing and war-risk exposure. Those with European inventory have pricing power for the first time in months, though the window may be narrow. Watch for the resumption of Asia-to-Europe flows once routing clarity and insurance markets normalize, that is when the structural price ceiling re-asserts itself.

The remaining integrated European producers, those with captive propylene oxide supply and flexible energy management, have a genuine competitive advantage in this environment. They have product. They have defined supply chains. They are not exposed to Hormuz rerouting risk on their feedstocks. The temptation will be to press that advantage on price, and the market would likely accept some increase given availability anxiety. The risk is overreaching: if the disruption resolves quickly and Asian volumes resume, any price gains will reverse sharply and relationship damage with key accounts will persist.

The deeper strategic question, beyond this crisis, is whether these closures and this disruption finally provoke a policy response that meaningfully addresses the energy cost differential. The European Commission's Chemical Action Plan and Clean Industrial Deal rhetoric has been positive; the concrete impact on production economics has been minimal. That calculus may be changing.

OUTLOOK: KEY FACTORS TO MONITOR

Given the rapidly evolving geopolitical environment, specific price forecasts remain highly uncertain. Instead, several key indicators should be closely monitored:

THE BOTTOM LINE

Europe's polyether polyol industry was already operating without a margin buffer when the Hormuz crisis began. The simultaneous shock to energy costs, feedstock logistics and import availability has removed the assumption of resilience that was still, however weakly, attached to remaining European production assets. The near-term price signal is upward, driven by anxiety, not demand recovery. The medium-term risk is that the disruption proves short-lived, Asian imports resume at low unit values, and the brief window of European producer advantage closes before any structural relief arrives. The permanent question, whether Europe retains a commodity polyol industry at all, has not been answered by this crisis. It has merely been made more urgent.

DATA NOTES & SOURCES

Polyol price data: PUdaily price assessments, Flexible Slabstock Polyols Bulk 3,000 MW, Spot, Western Europe, DEL, EUR/t. Price shown as mid-point of assessed range. | EU import data: Eurostat/UN Comtrade HS 390720 ("other polyethers, primary forms") — used as directional proxy; not identical to polyether polyol trade classification. | Energy data: TTF front-month, EIA STEO, Cefic. | Naphtha: Reuters, 4 March 2026. | Shipping: Drewry WCI, carrier notices. | Capacity data: company announcements. | Market colour: anonymised primary sources, 5 March 2026. | All scenarios in Chart 3 are illustrative cost-build estimates and do not constitute price forecasts.